For many elderly taxpayers in India, filing income tax returns every year can feel complicated and exhausting. Managing paperwork, understanding tax rules, keeping track of deductions, and navigating online filing systems can become increasingly difficult with age. Recognising this challenge, the Indian government introduced a special provision under Section 194P of the Income Tax Act to reduce the compliance burden for certain senior citizens aged 75 years and above.

Under this rule, some elderly taxpayers may not need to file Income Tax Returns (ITR) in FY27 if they meet specific conditions. However, the exemption is not automatic for every senior citizen. The relief applies only to a limited category of taxpayers with simple financial arrangements.

As awareness about the rule continues growing, many retirees and families are asking an important question: who exactly qualifies for this exemption, and how does it work?

What Is Section 194P?

Section 194P was introduced through the Finance Act, 2021 to provide tax filing relief to specified senior citizens. The provision allows eligible individuals aged 75 years and above to avoid filing income tax returns if their taxes are correctly deducted by a specified bank.

The objective behind the rule is simple: many elderly pensioners have straightforward income sources and should not be forced to go through annual tax filing procedures if taxes can already be managed automatically.

Instead of filing returns independently, eligible senior citizens can submit a declaration to their bank, which then calculates taxable income and deducts the required tax at source.

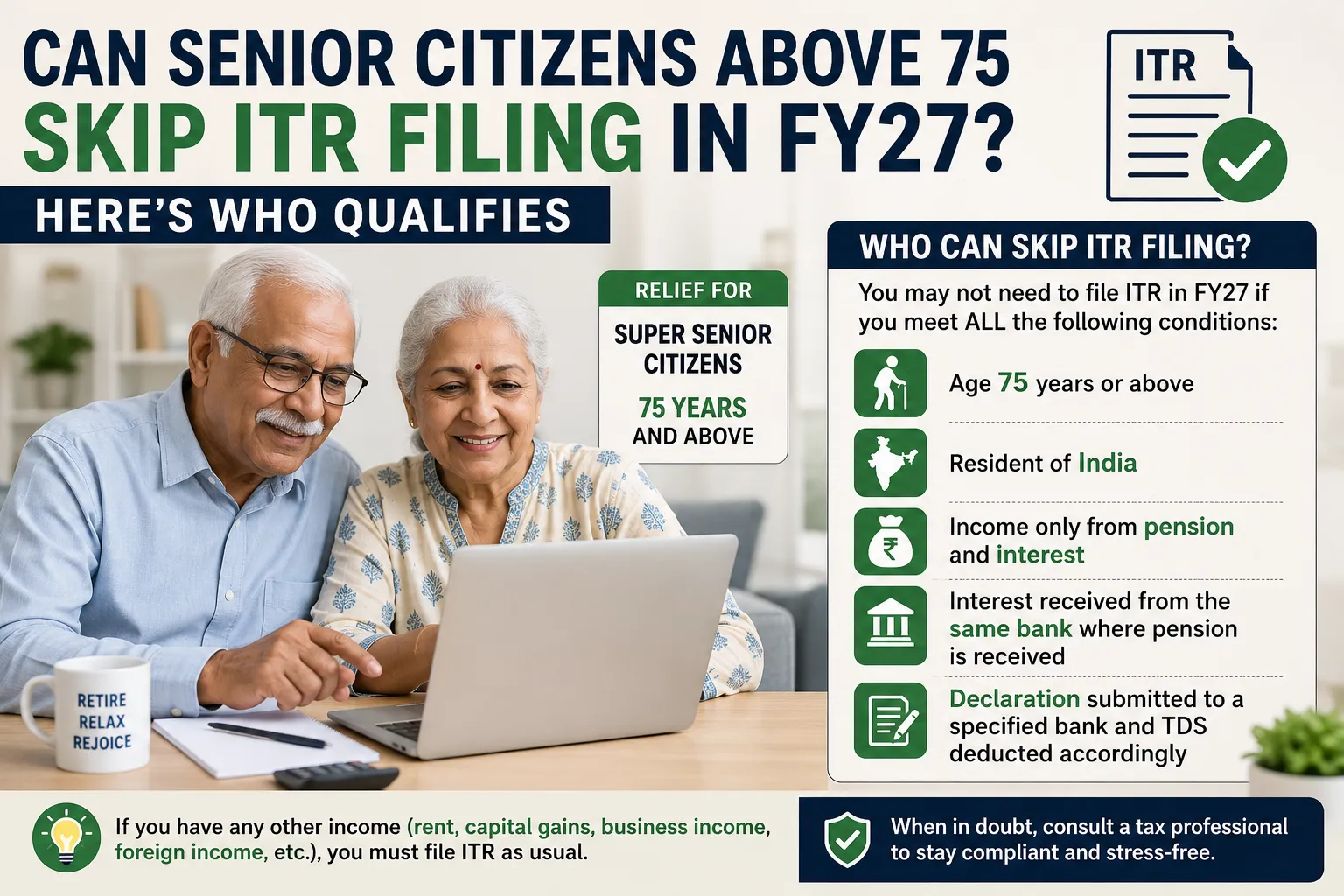

Who Is Eligible to Skip ITR Filing?

The exemption applies only when all prescribed conditions are satisfied.

Senior citizens aged 75 years or above may be eligible to skip Income Tax Return (ITR) filing under specific conditions. The individual must be a resident of India and should earn income only from pension and interest. The interest income must come from the same bank where the pension is received. The senior citizen must submit a declaration form to a specified bank. After this, the bank calculates the taxable income and deducts the required TDS. If all conditions are fulfilled and taxes are properly deducted, filing an ITR may not be necessary. However, additional income sources like rent, capital gains, or business income can make ITR filing mandatory again.

1. The Person Must Be 75 Years or Older

The taxpayer should be at least 75 years old during the relevant financial year. This rule specifically applies to elderly pensioners classified under the “specified senior citizen” category.

2. The Individual Must Be a Resident of India

Only resident senior citizens can avail this benefit. Non-resident Indians (NRIs), even if they are above 75 years of age, are not covered under this provision.

3. Income Should Be Limited to Pension and Interest

This is one of the most important conditions.

The senior citizen should have:

-

Pension income

-

Interest income only

The interest income must come from the same bank where the pension is received.

If the taxpayer earns income from:

-

Rent

-

Business

-

Capital gains

-

Multiple bank deposits

-

Mutual funds

-

Foreign assets

then the exemption may no longer apply.

4. Declaration Must Be Submitted to a Specified Bank

Eligible senior citizens must submit a declaration form to a notified “specified bank.” The bank then becomes responsible for calculating taxable income and deducting TDS accordingly.

The declaration generally includes:

-

Pension details

-

Interest income details

-

Deduction claims

-

Tax regime selection

Once the declaration is submitted and taxes are deducted properly, separate ITR filing may not be required.

How the System Works

Under Section 194P, the responsibility shifts significantly to the bank.

The process typically works like this:

-

The senior citizen submits the prescribed declaration

-

The bank calculates total taxable income

-

Eligible deductions and rebates are considered

-

TDS is deducted accordingly

-

The senior citizen becomes exempt from filing ITR

Banks are allowed to consider deductions under Chapter VI-A and rebate benefits under Section 87A while calculating taxable income.

This system is designed to simplify compliance for elderly taxpayers with uncomplicated financial situations.

Why the Government Introduced This Relief

The provision was introduced mainly to reduce the compliance burden on elderly citizens.

Many senior citizens:

-

Are unfamiliar with digital tax systems

-

Depend on family members for filing

-

Face health or mobility challenges

-

Have simple pension-based income structures

The government recognized that forcing such taxpayers to file returns every year despite limited income complexity created unnecessary hardship.

By allowing banks to manage tax deductions directly, the system aims to simplify life for elderly pensioners.

Why Many Senior Citizens Still File Returns

Even when eligible for exemption, some senior citizens may still choose to file ITRs voluntarily.There are several practical reasons for this.Many senior citizens continue to file Income Tax Returns even when they qualify for exemption because ITRs serve as important financial documents.

They are often required for visa applications, loan approvals, and investment-related processes. Filing returns also helps claim refunds if excess TDS has been deducted by banks. Some retirees have multiple income sources such as rental income, fixed deposits, or investments, making ITR filing necessary. Others prefer maintaining proper financial records for future security and transparency. Regular filing can also help avoid confusion or compliance issues later. For many elderly taxpayers, filing returns provides financial clarity and peace of mind.

1. Income Proof Requirements

ITRs are often needed for:

-

Visa applications

-

Loan approvals

-

Financial transactions

2. Refund Claims

If excess TDS is deducted, filing an ITR may help claim refunds.

3. Multiple Investments

Many retirees now invest in:

-

Mutual funds

-

Stocks

-

Rental property

-

Fixed deposits across multiple banks

Such investments may require normal tax filing anyway.

Common Misunderstandings About the Rule

A major misconception is that all senior citizens above 75 automatically become exempt from filing taxes.This is incorrect.A common misunderstanding is that all senior citizens above 75 years are automatically exempt from filing Income Tax Returns. In reality, the exemption applies only if specific conditions are fully met.

Many people overlook that the income must be limited to pension and interest from the same specified bank. Even small additional earnings like rental income, capital gains, or interest from another bank can make ITR filing mandatory. Some also assume the exemption works automatically without submitting any declaration form to the bank. Lack of awareness about these rules can lead to tax compliance issues. Therefore, senior citizens should carefully verify their eligibility before deciding not to file returns.

The exemption applies only if:

-

Income sources are limited

-

Interest comes from the same bank

-

The person is a resident

-

Required declarations are submitted

Even a small additional income source can affect eligibility.

For example:

-

Rental income

-

Capital gains

-

Interest from another bank

-

Foreign income

may make ITR filing mandatory again.

What Experts Often Advise

Tax professionals generally recommend that senior citizens carefully evaluate their financial situation before deciding not to file returns.

Experts suggest:

-

Reviewing all income sources annually

-

Confirming eligibility conditions properly

-

Maintaining financial records carefully

-

Consulting tax professionals if uncertain

Incorrect assumptions about exemption eligibility could create complications later.

How Retirement Income Is Changing

Retirement income patterns in India are changing significantly compared to earlier generations. Earlier, most senior citizens depended mainly on pensions and fixed deposits for financial security. Today, many retirees have diversified income sources such as mutual funds, stocks, rental properties, and multiple bank investments. Digital investment platforms have also encouraged senior citizens to explore modern financial options. As healthcare and living expenses rise, retirees are focusing more on wealth growth and passive income. This shift has made retirement finances more complex and has increased the importance of proper tax planning. As a result, many senior citizens may still need to file Income Tax Returns despite available exemptions.The modern retiree is financially different from previous generations.

Earlier, most senior citizens depended mainly on:

-

Pension income

-

Savings account interest

-

Fixed deposits

Today, retirees increasingly have:

-

Equity investments

-

Mutual funds

-

Rental income

-

Multiple bank accounts

-

Digital financial assets

This growing financial complexity means fewer senior citizens may fully qualify for the exemption compared to what many people assume.

The Importance of Tax Planning for Senior Citizens

Even after retirement, tax planning remains extremely important.

Senior citizens often depend on fixed income sources to manage:

-

Healthcare expenses

-

Household costs

-

Long-term savings

-

Emergency needs

Proper tax planning helps reduce unnecessary deductions and improve financial security.

Common tax-saving options for seniors may include:

-

Section 80C deductions

-

Health insurance deductions under Section 80D

-

Interest-related exemptions

-

Tax-efficient investment planning

Understanding these benefits can significantly improve post-retirement financial stability.

The Larger Push Toward Simplified Compliance

The exemption under Section 194P reflects India’s broader effort to simplify tax administration.

Recent reforms have focused on:

-

Automated tax systems

-

Pre-filled tax forms

-

Digital compliance

-

Faster refund processing

-

Reduced paperwork

At the same time, policymakers are also trying to make the system more accessible for elderly citizens who may struggle with technology-driven compliance systems.

Conclusion

The provision allowing certain senior citizens above 75 years to skip ITR filing offers meaningful relief, but only under carefully defined conditions. Eligible taxpayers must be resident Indians whose income is limited to pension and interest from the same specified bank, and they must submit the required declaration for tax deduction purposes.

While the exemption simplifies life for many elderly pensioners with straightforward finances, it is not a blanket exemption for all senior citizens. Even minor additional income sources may require normal ITR filing.

As India’s financial and tax systems continue evolving, measures like Section 194P highlight a growing effort to balance digital efficiency with compassion for elderly taxpayers. For senior citizens and their families, understanding these rules carefully is essential to ensure both compliance and financial peace of mind.

iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com iodailynews.com